Dear ETF Pro Subscriber,

Welcome back!

In this month’s edition of ETF Pro, we are removing long India (INDA) and rotating into Germany (EWG) on the short side.

With the INDA ETF registering a lower-high and failing to decisively recapture its intermediate-term TREND level after the recent burst of volatility, we think it’s time to rotate out of Indian equity exposure(s).

Importantly, the aforementioned financial market signal coincides with new signals emanating from our fundamental GIP Modeling framework, which now shows India slipping into #Quad3 here in Q1 instead of our previously forecasted #Quad2 outcome. India’s had a great run, but the cloudy growth outlook from here supports any decision to book gains.

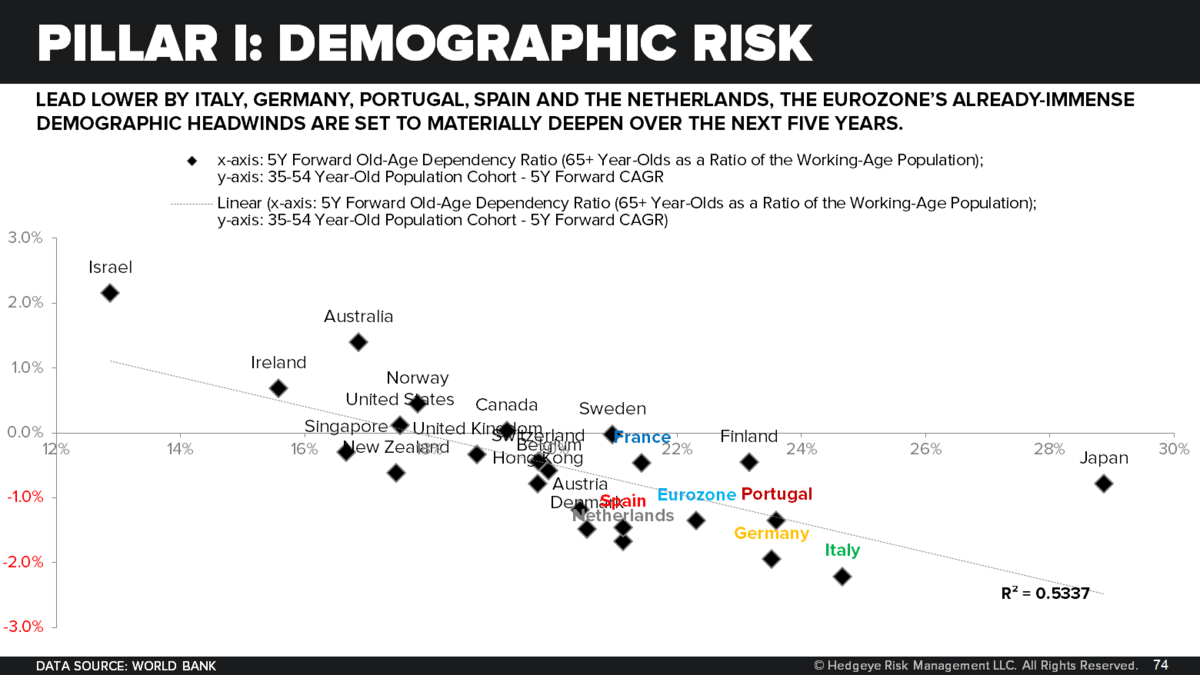

In conjunction with our Global Divergences and Europe Slowing themes, we continue to think Eurozone growth is on the precipice of a mid-cycle slowdown off of asymmetric peaks – seven year highs to be exact with respect to German economic growth.

Moreover, key high-frequency data – particularly on the consumption front, where consumption potential remains structurally challenged by demographic headwinds – is supportive of our #Quad4 outlook, at the margins.

Additionally, we think the EUR/USD cross will find it rather difficult to trade north of the 1.25 level implied by the top end of our 1.22-1.25 @Hedgeye Risk Range, which insulates our decision to short German equities on a currency-unhedged basis.

The U.S. dollar, which had gotten trounced by the recovery in global growth appears to be undergoing a bottoming process. It might actually look to make a series of higher-lows into and/or through the following calendar catalysts: FEB CPI on 3/13, MAR FOMC meeting on 3/21, and Q1 GDP on 4/27.

We reiterate our calls on the remaining 11 factor exposure biases currently highlighted in this edition ETF Pro.

Below is an updated list of the 12 current ETF Pro tickers. Keep reading for a detailed overview of these current ETFs, along with what we’ve added and removed since the last newsletter.

New users should definitely check out the Appendix for a brief primer on our Macro process and how we select (and remove) the exposures on ETF Pro. (CLICK HERE to review last month’s ETF Pro update.)

Here’s to another quarter of growth. Keep your head on a swivel,

–Darius Dale

Senior Macro Analyst

CURRENT ETF LINEUP

ETF CHANGES FROM LAST MONTH

COMMODITIES

No current high-conviction positions.

DOMESTIC EQUITIES

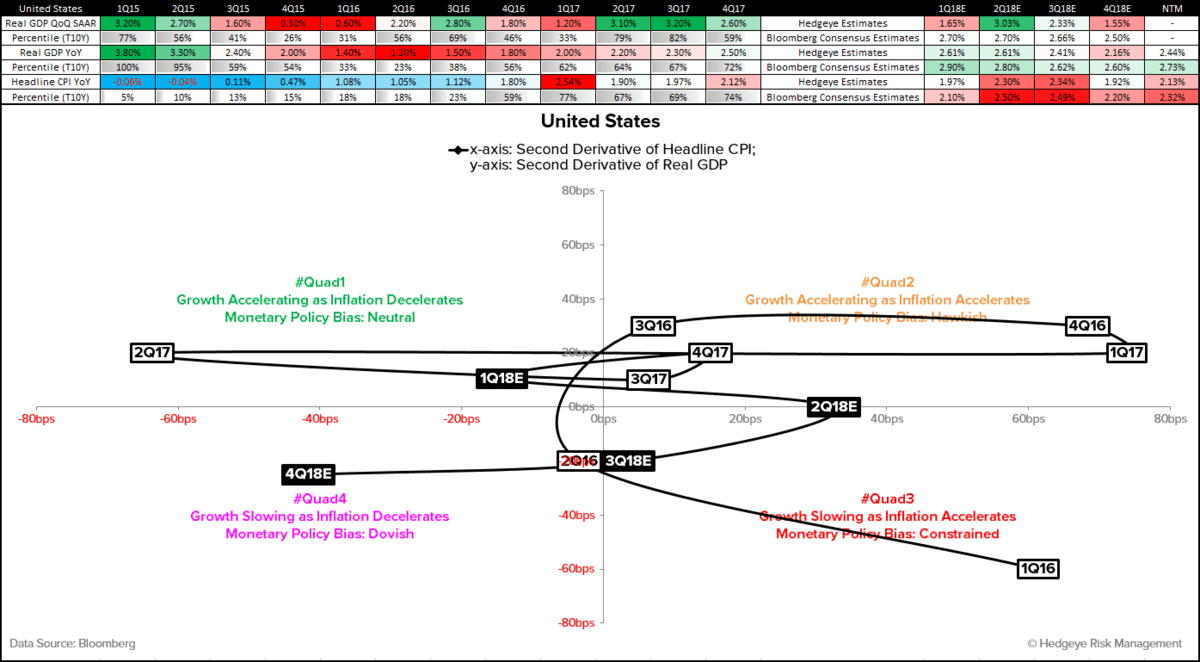

We are of the view that reported inflation peaked in Q4 and is set to surprise investors to the downside here in Q1. With growth continuing to accelerate throughout, pro QUAD 1 sectors and style factors like Technology, i.e. Nasdaq (QQQ), Biotech (IBB) and Consumer Discretionary stocks (XLY) should lead the way higher within the domestic equity market.

We also added U.S. IPOs (IPO) to squeeze incremental juice out of the eventual peak of the domestic economic and capital markets cycles.

While we don’t anticipate rates moving much higher from here over the next few months, we still think it pays to remain underweight defensive sectors like Utilities (XLU) and Consumer Staples (XLP) in line with our QUAD 1 playbook.

DOMESTIC FIXED INCOME

The aforementioned QUAD 1 regime should continue to remain positive for Convertible Bonds (CWB) and High-Yield Credit (JNK).

EMERGING MARKET EQUITIES

Colombian Equities (ICOL) is a great way to play a continuation of what has been sharply positive Emerging Market equity performance throughout the YTD, as its index profile (32% Natural Resources; 41% Financials) acts as a natural hedge for our Reflation’s Rollover II theme, while its favorable GIP Model setup (i.e. #Quad2 from 1Q18E-3Q18E) acts as a natural hedge for our Underweight EM theme.

In short, if Colombia doesn’t post a solid absolute return over the next 2-3 months, it’s likely because we’ll have been really right on our other preferred Long/Short factor exposures currently highlighted in this product.

FOREIGN EXCHANGE

No current high-conviction positions.

INTERNATIONAL EQUITIES

To reorient our favorite ETF ideas to this quarter's themes we added short South Korea (EWY) in the January edition of ETF Pro. Recall that we held a bullish bias on South Korean equities throughout most of 2017 en route to it outperforming both its DM and EM counterparts.

Now our GIP Model has South Korean growth and inflation negatively inflecting from ~3Y and ~5Y highs, respectively, in 3Q17 into a likely trend lower over the next few quarters. QUAD 4 is unlikely to prove positive for South Korean equities, which have steep implied volatility discounts – an explicitly bearish contra-indicator – on both a 30D and 60D basis.

Our model is prospectively signaling a concomitant deceleration in both economic growth and inflation across the broader Eurozone economy here in Q1.

We continue to think Eurozone growth is on the precipice of a mid-cycle slowdown off of asymmetric peaks – seven year highs to be exact with respect to German economic growth. Additionally, we think the EUR/USD cross will find it rather difficult to trade north of the 1.25 level implied by the top end of our 1.22-1.25 @Hedgeye Risk Range, which insulates our decision to short German equities (EWG) on a currency-unhedged basis.

Furthermore, we think downshifting beta at the sector and style factor levels is the appropriate risk to take, which effectively means short of Italy (EWI) – which is likely to experience its second consecutive quarter of QUAD 4 here in 1Q18E – and its elevated exposure to Financials of 35% and awful demographics.

INTERNATIONAL FIXED INCOME

No current high-conviction positions.

APPENDIX

We find two factors to be most consequential for forecasting future financial market returns: economic growth and inflation. We track both on a year-over-year rate of change basis to better understand the big picture then ask the fundamental question: Are growth and inflation heating up or cooling down?

From there, we get four possible outcomes, each of which is assigned a “quadrant” in our Growth, Inflation, Policy (GIP) model and the typical government response as a result (neutral, hawkish, in-a-box or dovish): Growth accelerating, Inflation slowing (QUAD 1); Growth accelerating, Inflation accelerating (QUAD 2); Growth slowing, Inflation accelerating (QUAD 3); Growth slowing, Inflation slowing (QUAD 4).

After building this base of knowledge, we can now select what we like and don’t like based on our historical back-testing of the different asset classes that perform best in each of the four quadrants. As you can see in the chart above, our GIP model suggests that the U.S. economy is likely to rotate back to #Quad1 in the first quarter of 2018. This has historically been the best economic regime for domestic equities.

Below is a chart that lays out precisely what we like and don’t like when an economy is in each of the four quadrants. This chart should help you make better investment decisions, even outside our recommendations in ETF Pro.

{kind=link}