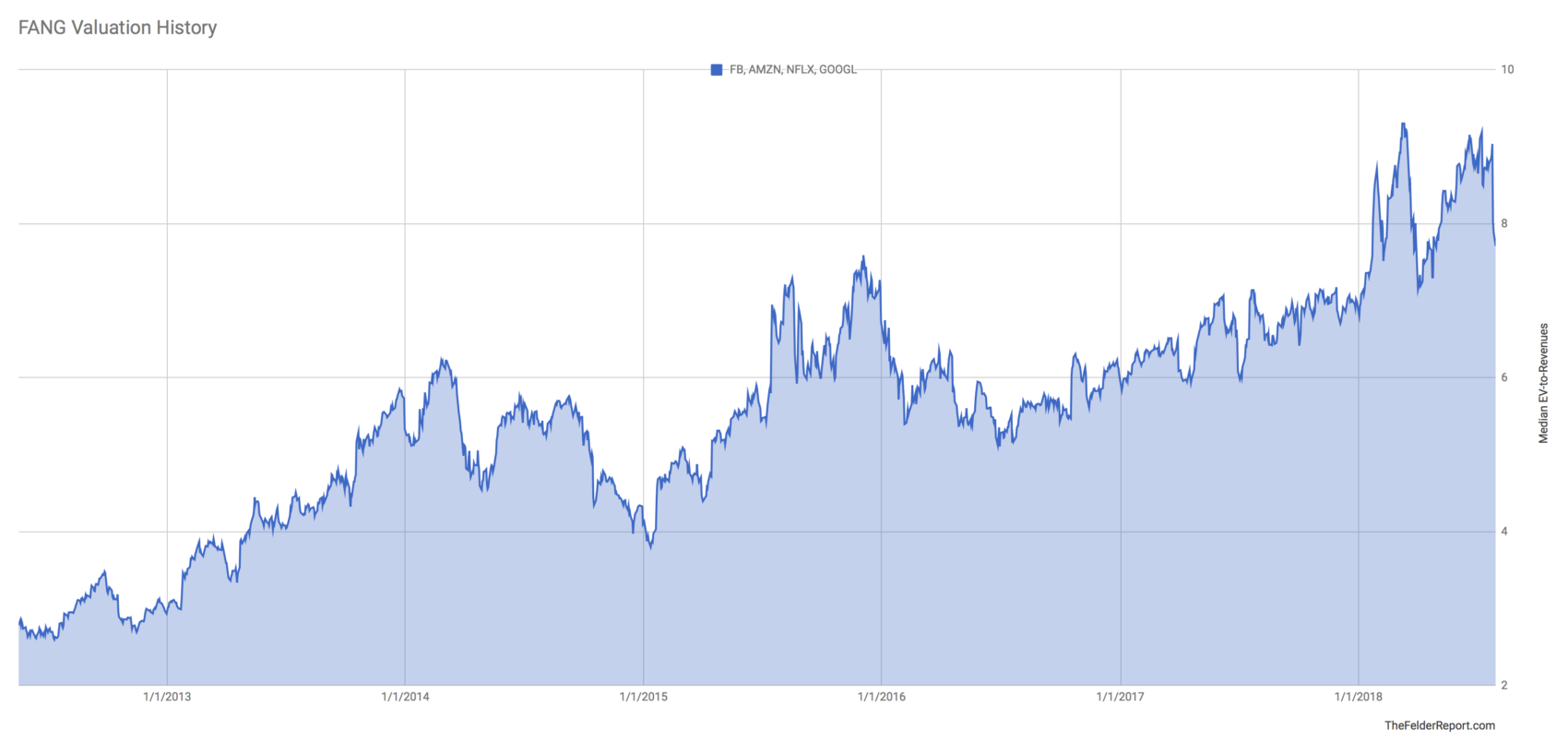

With the FANG stocks faltering lately investors are starting to become concerned about their impact on the broader market. And there is certainly something to this. Statistically speaking, these market generals have become increasingly important to the broad market indexes recently so it only stands to reason that an important reversal here could make for a more difficult equity environment in general.

And it’s certainly true that, as Howard Marks pointed out recently, these four are currently priced for perfection just as perfection begins to look more and more like a mirage. The reckoning between euphoric investor expectations and what these companies are actually capable of delivering could make for a much larger decline in their share prices as a group should their valuations reset to anything close to their averages in recent years.

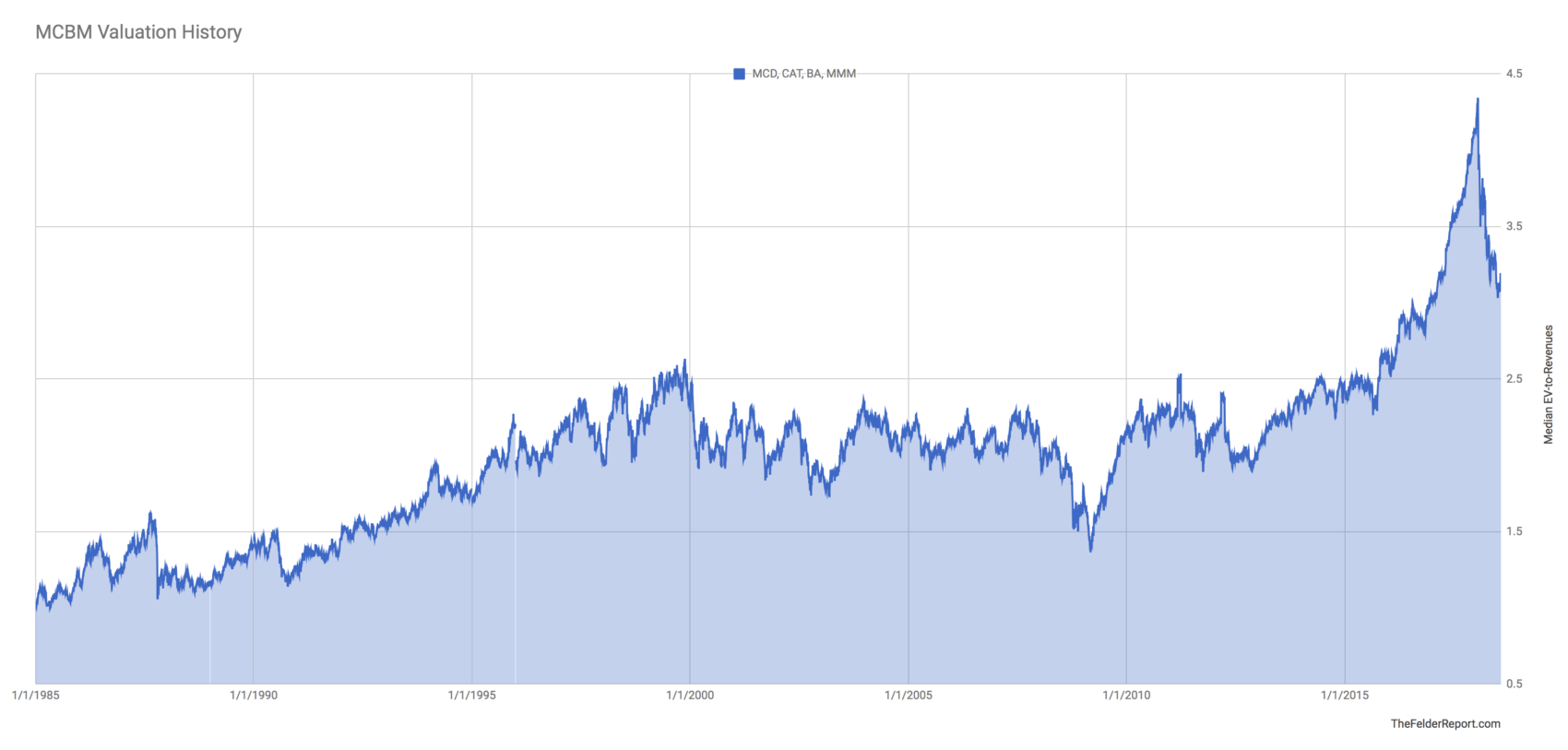

But it’s important to remember that it’s not just the FANG stocks that are vulnerable to a repricing due to their record-high valuations. As I wrote earlier this year, there is another fantastic four made up of much more boring blue chip stocks that even outperformed the FANGs last year. MCBM, as I have termed the group, has a much longer financial history that gives greater perspective to the recent valuation extreme.

These stocks have been faltering for months now even as the FANG stocks have continued to climb. It appears investors have been reappraising their euphoric assumptions for this group since the start of the year. Here again, should valuations return to anything close to normal the downside for their share prices is still significant.

Finally, I would just point out that this phenomenon of extreme valuations driven by euphoric assumptions is far more pervasive than just these two quartets would suggest. The median price-to-sales ratio on the S&P 500 currently stands at an unprecedented extreme. And even if we take an index like the Dow Jones Industrial Average, which includes not one FANG stock, the message remains: investor euphoria, as manifest in equity valuations, is more extreme and more pervasive than ever before.

What investors really should be worried about then is the possibility that the reappraisal of the FANG stocks is representative of a much wider reappraisal that began back in February. Because if the heroic assumptions behind these unprecedented valuations are not met the repricing for not just the FANGs or MCBM but the entire stock market could be significant.

What investors really should be worried about then is the possibility that the reappraisal of the FANG stocks is representative of a much wider reappraisal that began back in February. Because if the heroic assumptions behind these unprecedented valuations are not met the repricing for not just the FANGs or MCBM but the entire stock market could be significant.