“When it comes to investing, it’s a losing proposition to try and be anything better than average.

If there’s no point in trying to beat the market through ‘active’ investing – using mutual funds that managers run, selecting what they hope are market-beating investments – what is the best way to invest? Through “passive” investing, which accepts average market returns (this means index funds, which track market benchmarks)” – Forbes

The idea of “passive indexing” sounds harmless enough, buy an “index” and be an “average” investor.

However, it isn’t as simple as that, and we have spilled a lot of ink digging into the relative dangers of it. Last week, investors saw those risks first hand.

The biggest risk to investors is when “passive indexers” turn into “panic sellers.”

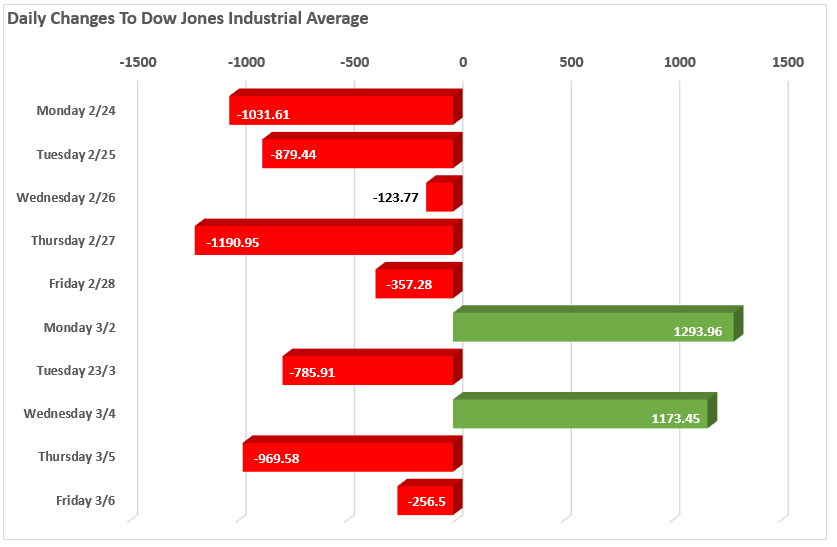

While the “sell-off” over the last couple of weeks was brutal, with the Dow posting some of the biggest declines in its history, as I will explain, it was exacerbated by the “passive indexing revolution.”

Jim Cramer previously penned (courtesy of Doug Kass) an interesting note on the active vs. passive conflict.

“The answer is that there are two kinds of sellers in this market: hedge fund sellers, who react off of research, and portfolio shufflers, who buy and sell ETFs and index funds.

The former jumps on anything, right or wrong, as long as it is actionable. The latter, the index funds and ETF traders, rarely jump although they may press down harder on a bedraggled ETF, like one that includes the consumer products group.

But there are two kinds of buyers. The opportunistic buyers, and the index buyers. The opportunists think that the downgrades are noise and give them a chance to buy high-quality stocks with the money that comes in over the transom.

The index and ETF buyers? Well, they just buy.”

The dichotomy explains a lot of the bullish action, and isn’t talked about enough.

While Jim wrote this about those “buying” ETF’s, the same is true when they begin to “sell.”

“The index and ETF sellers? Well, they just sell.”

It is often suggested that individuals who buy “passive indexes,” such as the SPDR S&P 500 Index (SPY), are they themselves “passive investors.” In other words, these individuals are willing to buy an “index” and hold it for an extended period regardless of market volatility.

Reality has been far different.

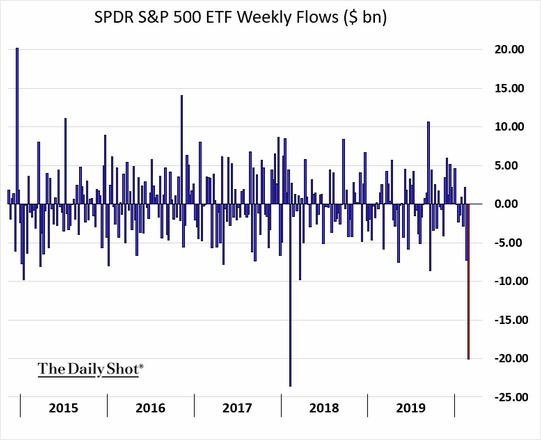

This was clear last week as the S&P 500 ETF (SPY) saw some of the biggest outflows in its history with the exception of the February 2018 market plunge as Trump announced his “Trade War with China.”

The problem with individuals and “passive” investing is they are just “active” investors in a different form. They make all the same mistakes that individual stock investors make, such as “buying high and selling low,” but just using a different instrument to do it.

As the markets declined last week, there was a slow realization “this decline” was something more than another “buy the dip” opportunity. Concerns of the impact on the global supply chain, due to “COVID-19,” slowing earnings, economic growth, and a reduction of liquidity from the Federal Reserve, all culminated in a “panicked exit.”

As losses mounted, anxiety rose until individuals began to sell to “avert further losses” by selling.

Yes….it’s that psychology thing.

Individuals refuse to act “rationally” by holding their investments as losses mount.

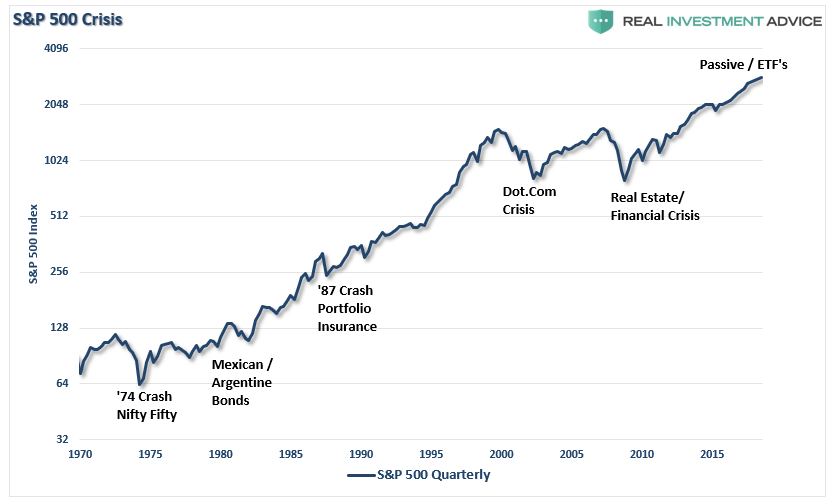

The behavioral biases of investors are one of the most serious risks arising from ETFs as too much capital is concentrated into too few places. This concentration risk in ETF’s is not the first time this has occurred:

- In the early 70’s it was the “Nifty Fifty” stocks,

- Then Mexican and Argentine bonds a few years after that

- “Portfolio Insurance” was the “thing” in the mid -80’s

- Dot.com anything was a great investment in 1999

- Real estate has been a boom/bust cycle roughly every other decade, but 2007 was a doozy

- Today, it’s ETF’s and Bitcoin

Risk concentration always seems rational at the beginning, and the initial successes of the trends it creates can be self-reinforcing.

Until it goes in the other direction.

While the sell-off last week was large, it was the uniformity of the price moves, which revealed the fallacy “passive investing” as investors headed for the exits all at the same time.

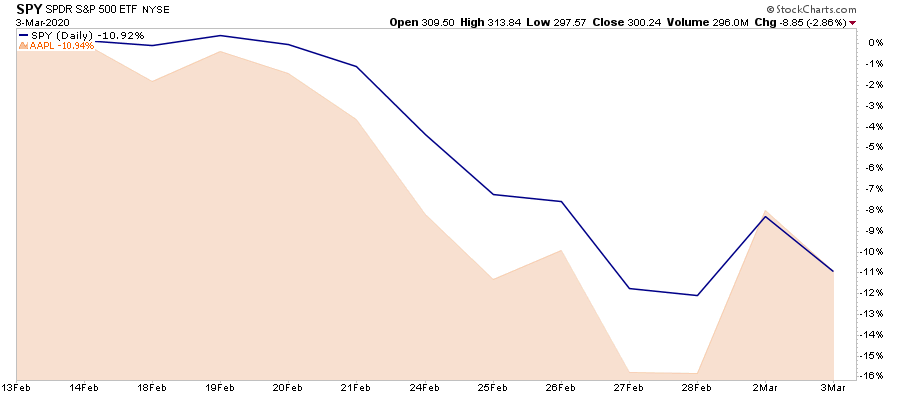

The Apple Problem

Currently, there more than 1750 ETF”s trading in the U.S., with each of those ETF’s owning many of the same underlying companies. For an ETF company to “sell” you product, they need good performance. In a late-stage market cycle driven by momentum, it is not uncommon to find the same “best performing” stocks proliferating a large number of ETF’s.

For example, out of the 1750 ETF’s in the U.S., there are 175, or 10%, which own Apple (AAPL). Given that so many ETF’s own the same company, the problem of “liquidity” is exposed during a market rout. The head of the BOE, Mark Carney, warned about the risk of “disorderly unwinding of portfolios” due to the lack of market liquidity.

“Market adjustments to date have occurred without significant stress. However, the risk of a sharp and disorderly reversal remains given the compressed credit and liquidity risk premia. As a result, market participants need to be mindful of the risks of diminished market liquidity, asset price discontinuities and contagion across asset markets.”

Howard Marks, also noted in ‘“Liquidity:”

“ETF’s have become popular because they’re generally believed to be ‘better than mutual funds,’ in that they’re traded all day. Thus an ETF investor can get in or out anytime during trading hours. But do the investors in ETFs wonder about the source of their liquidity?’”

Let me explain.

There is a statement often made by individuals about the market.

“For every buyer, there is a seller.”

The belief has always been that if an individual wants to sell, there will always be a buyer available to execute the transaction at any given price.

However, such is not actually the case.

The correct statement is:

“For every buyer, there is a seller….at a specific price.”

In other words, when the selling begins, those wanting to “sell” overrun those willing to “buy,” so prices have to drop until a “buyer” is willing to execute a trade.

The “Apple” problem, using our example above, is that while investors who are long Apple shares directly are trying to find buyers, the 175 ETF’s that also own Apple shares are vying for the same buyers to meet redemption requests.

This surge in selling pressure creates a “liquidity vacuum” between the current price and the price at which a “buyer” is willing to step in. As we saw last week, Apple shares fell faster than the SPDR S&P 500 ETF, of which Apple is one of the largest holdings.

Secondly, the ETF market is not a PASSIVE MARKET. Today, advisors are actively migrating portfolio management to the use of ETF’s for either some, if not all, of the asset allocation equation. Importantly, they are NOT doing it “passively.” The rise of index funds has turned everyone into “asset class pickers,” instead of stock pickers. However, just because individuals are choosing to “buy baskets” of stocks, rather than individual securities, it is not a “passive” choice, but rather “active management” in a different form.

While “passive indexing” sounds like a winning approach to “pace” the markets during the late stages of an advance, it is worth remembering it will also “pace” just as well during the subsequent decline.

The correction had the “perma-bulls” scrambling to produce commentary as to why markets will continue only to rise. Unfortunately, that is not the way markets actually work over the long-term, and why the basic rules of investing are REALLY hard to follow.

Despite the best of intentions, individual investors are NOT passive even though they are investing in “passive” vehicles. When these market swoons begin, the rush to liquidate entire baskets of stocks accelerate the decline making sell-offs much more violently than what we have seen in the past.

This concentration of risk, lack of liquidity, and a market increasingly driven by “robot trading algorithms,” reversals are no longer a slow and methodical process but rather a stampede with little regard to price, valuation, or fundamental measures as the exit becomes very narrow.

February was just a “sampling” of what will happen to the markets when the next bear market begins.

Are you prepared?

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors. He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Also Read