A dead rat would’ve easily explained the foul odor, though it wouldn’t have ended the matter. The smell was real, the cause still yet to be identified in the mainstream view. For the bond market, anyway, it was a process of discovery which began with an unexpected stench of something much bigger and more profound than any single or simple rodent (dead or alive).

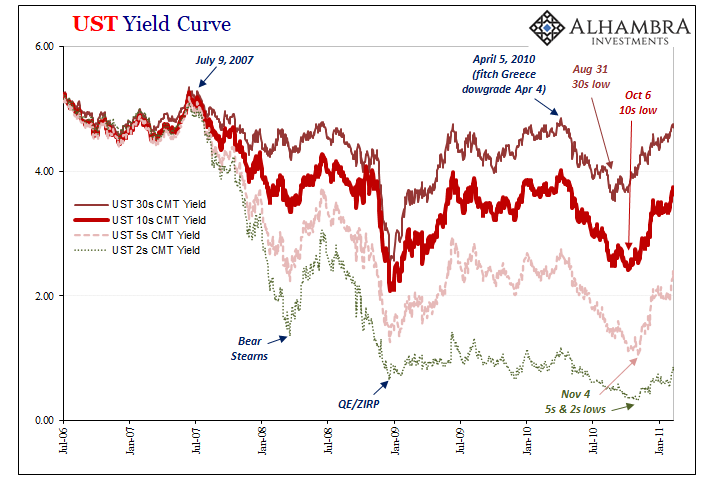

This was April 2010, an extremely crucial month setting up what would become – over time – several fallacies that have struggled under this weight of contradictory reality. The world was, everyone said, recovering from the Great “Recession” mercifully ended not even a year before due to the combined heroics of central bankers and fitful government spendthrifts (though mostly the former, who took all the press and credit, with their “novel” application of non-standard monetary “accommodation” in the form of QE).

Then that relatively small European nation otherwise imperceptibly nestled into the Mediterranean landscape “somehow” started to derail everything.

On March 4, 2010, the Greek government celebrated market acceptance of its initial “austerity” proposal when its 10-year bond sale went off like gangbusters. The salutations quickly soured as only twenty-five days later a 7-year GGB auction failed to attract nearly as much cheerfulness. Then on April 4, Fitch downgrades Greek credit to BBB- and suddenly…US Treasury yields begin to plummet?

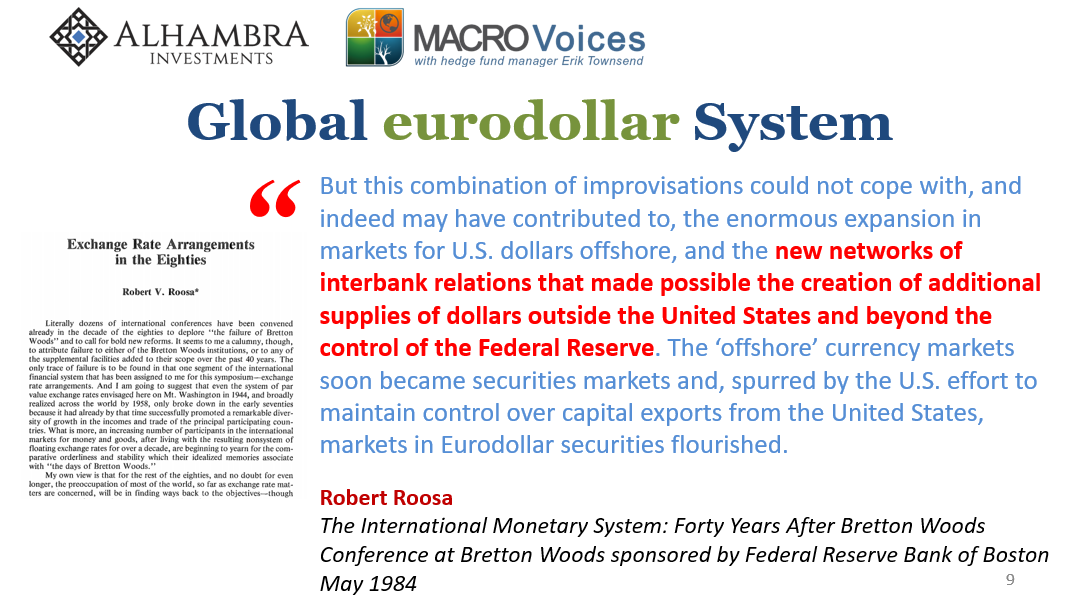

Yes, but several steps remain unidentified, to this day, in between. German and French government bonds had already been trading slightly “special” in European repo prior to April; with the fireworks after the fourth, those began to trade more (steadily) special joined by Belgian bonds (and initially, get this, Italian sovereign!)

What that had signaled was collateral shrinkage and thus extra pressure on bond types which would have been steadily negotiable in repo markets; out with Greek bonds herding everyone formerly using them into the better alternates. If only gross collateral switching and haircutting could be so simple and easy rather than – as the world should’ve realized in September and October 2008 – destructively disruptive.

The fuse had been (re)lit, however, and by the end of April 2010 euro repo was a total mess and well on its way to becoming an unmitigated as well as systemic disaster. Early on in May, well, you can read those details here.

Before everything, meaning global recovery, really began to fall apart, back when Greece was being cheered for its austerity, judging in bonds there was already priced substantial skepticism about that view. Rates should have been moving far more briskly at least back to where they’d begun the Global Financial Crisis (why and how was it global, again?) but remained instead stubbornly and noticeably less than their pre-crisis launch point.

The global recovery was proceeding, but there was this nagging worry over how it wasn’t really a recovery. Too many questions were left, too many unsolved “riddles” like Greece and its effects on global repo. Despite Ben Bernanke’s most illustrious efforts, as early as March 2010 some instead had smelled a rat.

In the absence of any major economic data Tuesday, the Treasury market is merely moving based on the 10-year note auction, said Michael Cheah, a bond fund manager for SunAmerica…The market is diluting itself on this news but the calming effect could wear off, Cheah said. “Nobody wants to talk about this giant dead rat under the carpet,” he said.

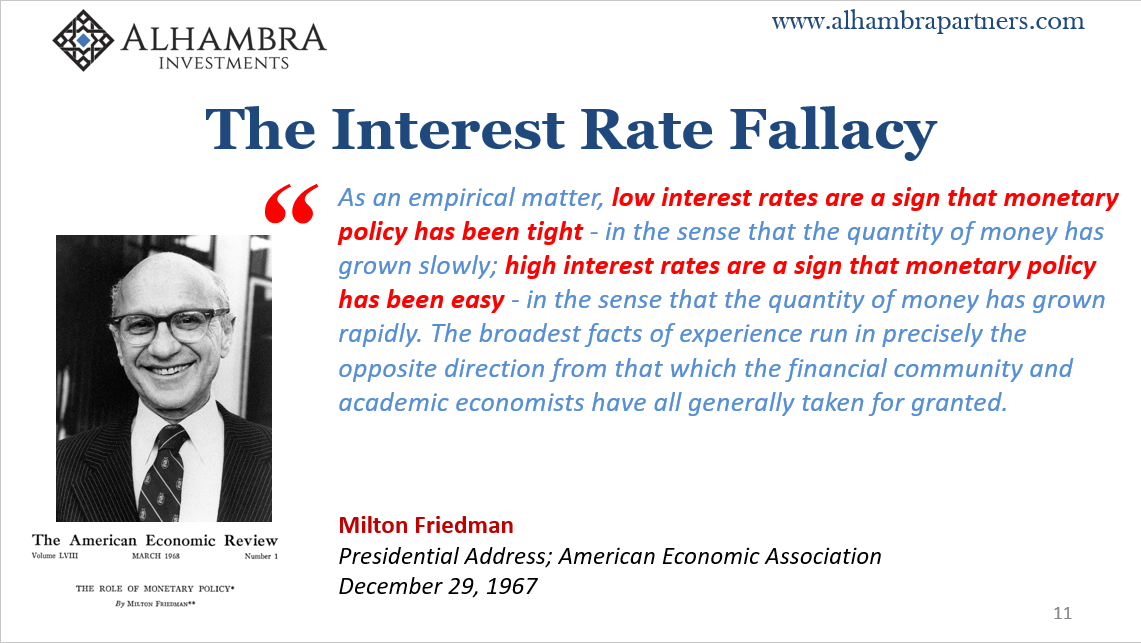

Some people still claim that QE is money printing, that it creates “liquidity.” But even if it doesn’t, even if there isn’t any money spit out of its printer, then at the very least it must be reducing bond yields and keeping them down. After all, this is bond buying we’re talking about and in almost every case the central bank buying up the bonds does so in enormous quantities.

Yet, following more than a decade of practice and nearly as much academic and central bank scholarship examining the results, very little of this is ever detected. At most, the studies all say that maybe, perhaps QE reduces bond yields only a little bit more than the huge chunk the market already has at each juncture.

Forget the “studies”; see for yourself. These academic investigations (often purposefully) employ the most charitable methodology and still it’s underwhelming. Observing instead actual experience, it’s almost a near opposite which confounds all the models and conventional expectations if only because of the interest rate fallacy. Furthermore, yield behavior has evolved considerably over the nearly thirteen years of global usage.

Already, from the very early days of the crisis, the interest rate fallacy has continued to defy in full view. From July 2007, yields began falling not because the market was anticipating Ben Bernanke to reverse course and start cutting rates (which he eventually did) but rather due to the looming, enormous consequences of a once-in-four-generations (allegedly) hit to finance and economy, and what that’d likely do to growth and inflation (not to mention repo and effective money).

Even during the crisis itself, yields were already moving the opposite as the conventional view had it; from Bear Stearns, for example, yields rose as the bond market gave Bernanke’s early crisis rescues a partial vote of confidence if only to turn right around reversing to lower again from June 2008.

Perhaps most striking of all, the crisis lows for UST’s were registered at the Fed’s December 2008 announcement of ZIRP/QE. In other words, again the benefit of the doubt over “new” non-standard practices, interest rates rose not fell once the US central bank declared its intentions to buy bonds.

The market was simply saying, this new stuff might work.

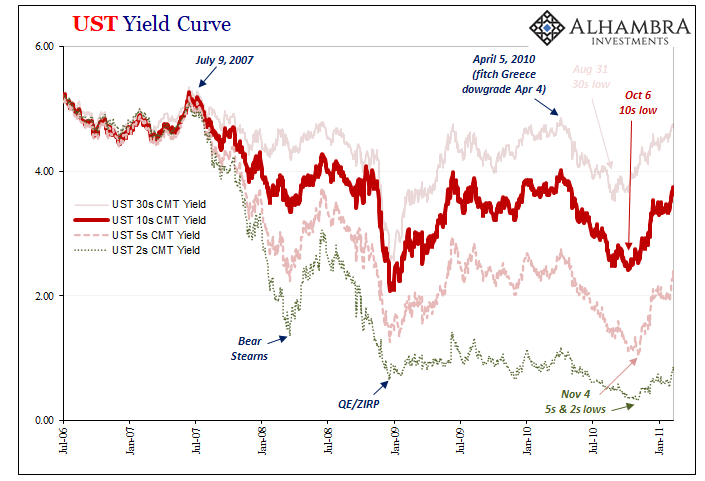

Skepticism, however, crept into global not just US bonds later in 2009. Inside the 30-year long bond, yields never did get back to their pre-crisis highs and, taking note of the increasingly dramatic rodent stench, yields lurched lower throughout the middle of 2010 not because of QE1 in the US (or whatever other things the ECB was doing) but because of renewed trouble and crisis even if that trouble seemed to have been isolated in Europe.

Repo market tightening of collateral pools, in reality, was never strictly about “over there.”

Rates began to turn around at the end of August 2010 when Ben Bernanke appeared at Jackson Hole in Wyoming to profess his guarded interest in a second QE by issuing the now-standard qualifier “if conditions warrant.” On that wink and a nod toward a second massive bond buying program, long-term yields first at the 30-year maturity like before began to rise rather than fall. These were joined six weeks later in early October by the UST 10-year and then short-term instruments on November 4 when QE2 was eventually announced.

Again, backward to convention – more bond buying, higher rather than lower yields because the market, at that time, was somewhat more forgiving about the potential one of these things might actually become successful. And if one ever did work, then inflation and growth go up, and that is what drives bond yields.

Inflation and growth potential.

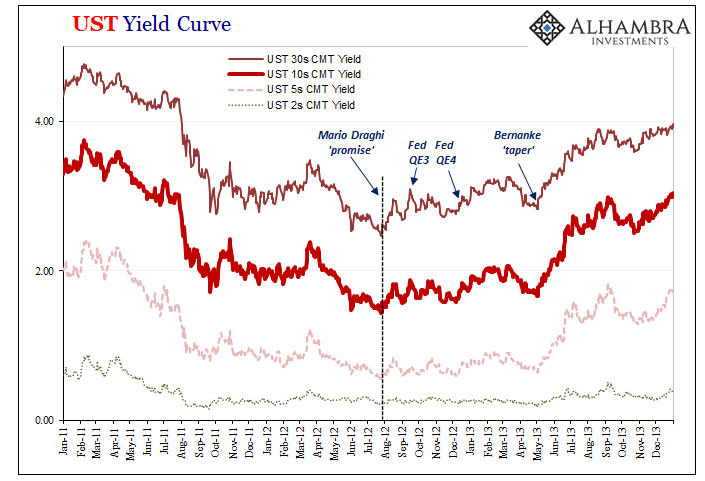

The next QE episode, I believe, really drives home what has become inflation and growth skepticism; the evolving viewpoint more and more established after each practice. Following the perhaps inevitable fallout from what began as “Greek bonds”, a second global crisis erupted in the middle of 2011 (Euro$ #2) which pushed UST as well as global yields even further downward. Again, not the result of bond purchasing central bankers, the reaction to renewed (severe) tight money as well as the negative effects that would have (and did have) on inflation and growth.

What eventually turned those yields around was…a vague promise by Europe’s top central banker, Mario Draghi, in July 2012 to do something that had nothing directly to do with bond buying anywhere. His commitment to “do whatever it takes” to save the euro was merely a blank canvas addition to the central bank toolkit, something potentially different (if only because it wasn’t specified) that could bring the world economy back on course (presuming, as many did, that if the “thing” was broken in Europe then Europeans would have to first fix it).

Truly remarkable, then, how little response in the marketplace (not just UST’s) to the Federal Reserve in September 2012 announcing QE3 (buying only MBS) and then the same lack of movement when Bernanke’s policymakers redoubled it with QE4 (buying USTs) that December.

This marked an enormous and enormously important contrast with the market responses following first QE1 and even QE2. Bonds were now starting out visibly skeptical about monetary (especially repo) conditions globally therefore growth and inflation when it came to these policies.

Heading toward the middle of 2013, bonds were saying, essentially, there’ll be no more benefit of the doubt, we demand evidence first.

What finally moved yields upward, while QE4 was still ongoing, was the misunderstood and therefore misidentified “taper tantrum” in early May 2013. By that point, Europe seemed poised to move out of its 2011-12 re-recession while in the US it more and more looked like the American economy would avoid one and set up a more plausible path to recovery.

When Bernanke said “taper” (though he didn’t actually use the word), he was really saying that even cautious Fed officials were starting to believe in the recovery story, zooming in on evidence of it (fast falling unemployment rate) and that’s why the word “taper” had so much more of an effect on bond yields (in a good way) than either QE3 or QE4.

It did not last very long, by September 2013, at the earliest, and December yields peaked and spent 2014 moving back lower again at the same time the Fed actually tapered its bond buying and then terminated it entirely. Almost completely backward.

Why the need for this QE review?

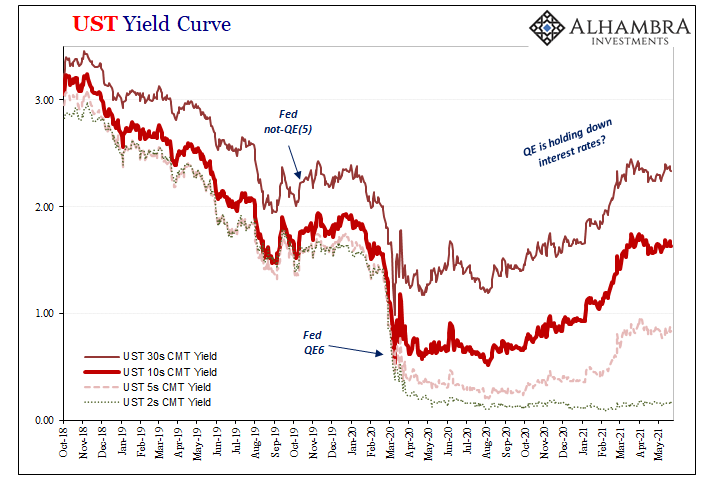

Because even today you continue to hear how it is central bank bond buying which is right now responsible for holding down yields, and that because QE’s keeping rates low we can just throw them out for any sort of useful financial and economic signal as an artificial product of intentional and even helpful monetary policy.

As we can easily see, however, absolutely none of that is true nor has it been from the very beginning. Yields go up when the market believes there might be a better chance of growth and inflation (less tight money) at times (more in the early crisis aftermath) conflating central bank policies with more positive chances. But then yields go down when it becomes painfully clear there really aren’t (m)any positives.

What the nearly forgotten Greek episode established/proved/reminds us are these global factors to money therefore inflation and recovery. When UST yields plunged in April 2010, it wasn’t because of troubles in Greece nor was it bond buying here or anywhere (QE1 had ended on March 31, actually), it was because global market money players realized what havoc money troubles in repo would cause for the entire global system.

Right now, bond yields around the world are incredibly low which means, like at these points in the past, they aren’t seeing anything different let alone modest inflation if anything like it becoming simply overwhelming in our near future. Furthermore, they’ve barely budged even after the epic, biblical price surge embedded within last month’s CPI (and PPI).

Is this because of central bank bond buying? Or, bonds still smell the same dead rat?

Maybe, too, these long-deceased vermin are of a special kind, a sort of bellwether species. Repo rats. The reasons to be inflation-skeptical presented by stubbornly low yields are indeed related to QE bond buying, if only in how QE bond buying (or anything else including out-of-control government spending) doesn’t ever work and that interest rates really do work the opposite way of mainstream commentary (the fallacy).

Stay In Touch